“Precious” has been working in Hong Kong as a domestic helper for two years now. In July of 2016, she was forced to make a loan of HK$ 13,000 because of two emergencies. Back home, in the southern Philippines’ city of Pagadian, her husband’s body was numbing, and her only child’s blood platelets were dropping rapidly due to Dengue virus. She doesn’t have immediate cash for their hospitalization and borrowing money from credit companies was the only solution she could think of. Today, after nine months of budgeting HK$ 1,585 every month from her salary, she’s about to finish paying her loan. She is thinking of borrowing money again to build their own house in the Philippines.

“Trina,” another Filipina domestic helper in Hong Kong for 13 years now, also made a loan last year for her sister’s placement fee in Canada. She borrowed HK$ 40,000, payable within 18 months with monthly interest of 1.69 percent. Majority of her HK$ 4,500 salary every month goes to loan payment, and the rest is sent to her family in the Philippines. She said she just need HK$ 30 every Sunday when she goes to church. She’s living in her employer’s flat and food is provided.

“Maria’s” case is different. She did not intend to borrow money, but in 2014, out of debt-of-gratitude to another domestic helper who financially helped her before, she agreed to vouch for her when the latter borrowed HK$ 40,000 to a Filipina moneylender. Soon her friend left Hong Kong for Russia, leaving Maria the responsibility of paying. She was not able to pay the moneylender, as she was also paying a personal loan in the Philippines at the same time. The amount loaned spiked to HK$ 100,000 due to non-payment and accumulation of interest. She was harassed, threatened, and intimidated. She sought help from the Philippine Consulate General in Hong Kong and the Mission for Migrant Workers (MFMW). Her case remains unresolved up to now.

The stories of Precious, Trina, and Maria are just microcosms of the growing concern of hundreds of thousands of migrant domestic helpers in Hong Kong – debt. Enrich HK, a local charity promoting economic empowerment of migrant domestic workers, estimates 51 percent of helpers in Hong Kong struggle with debt, and the numbers continue to rise as more migrant workers arrive each year to work in Hong Kong.

In some cases, helpers have exhausted all possible sources of loans to pay for other outstanding loans, and debts pile one after another, and they hardly make the ends meet, thus loans accumulate interests beyond their capacity to pay. These give the loan sharks chance to harass and intimidate the helpers and their employers to force payment, leading to eventual termination of the helpers’ contracts, depression, and sometimes suicide.

The Root Cause of Helpers’ Debts

According to MFMW’s General Manager Cynthia Abdon – Tellez, domestic helpers get buried in debt because they are already in debt even before coming to Hong Kong.

“Although the Philippine government scrapped the placement or agency fees in December 2006 for outgoing Overseas Filipino Workers (OFW), they mandated that helpers should undergo skills and language training and other seminars prior to their employment. These trainings, conducted by placement agencies, do not have ceiling prices for training rates and can range from PHP 5,000 to PHP 100,000 (HK$ 800 – 16,000). Where will they get that amount?” said Tellez.

Historically, according to her, moneylenders started to mushroom during the mid-1980s when Philippine Pres. Ferdinand Marcos made a force remittance order to all land-based OFWs to help the ailing economy of the country. Migrant workers were obliged to remit 50 percent of their monthly salary to their families back home through some specific banks in the Philippines, and failure to comply means non-renewal of their passports. Passports during that time expire every two years. Some OFWs thought it would be easy to make a one-time payment before their contracts end, only to find out it was a struggle to produce the amount required by the Philippine government for them to renew their passports and contracts. Thus, they resorted to moneylenders.

More loan sharks proliferated in the succeeding years when placement agencies charged exorbitant placement fees to Filipinas seeking greener pastures in Hong Kong.

“They have their way to toy around our law,” said Tellez, referring to placement agencies’ tactics to extract more money from unsuspecting applicants to Hong Kong.

“They would lure the applicants to faster processing of applications but would ask for additional payment, say PHP 30,000. If the applicant does not have money at that moment, they would offer loans from partner moneylenders, but would force the applicant to open a checking account and issue post-dated blank checks,” she added.

The employment agency and its partner financing firm are the ones who decide what to write in the check.

Bounced check, or checks issued without enough funds on the specified date, is estafa, a criminal case in the Philippines.

Sometimes, helpers incur loan without their knowledge.

“When they (domestic helpers) leave the Philippines, or Indonesia, recruitment agencies promise them that everything has been taken care of, only to find out that they have been charged when they reach Hong Kong. It is considered as loan,” said Tynna Mendoza, program manager of Enrich HK.

Tellez also said that around 80 percent of the total salary of domestic helpers are paid to conniving moneylenders and employment agencies, leaving nothing to send to their family back home.

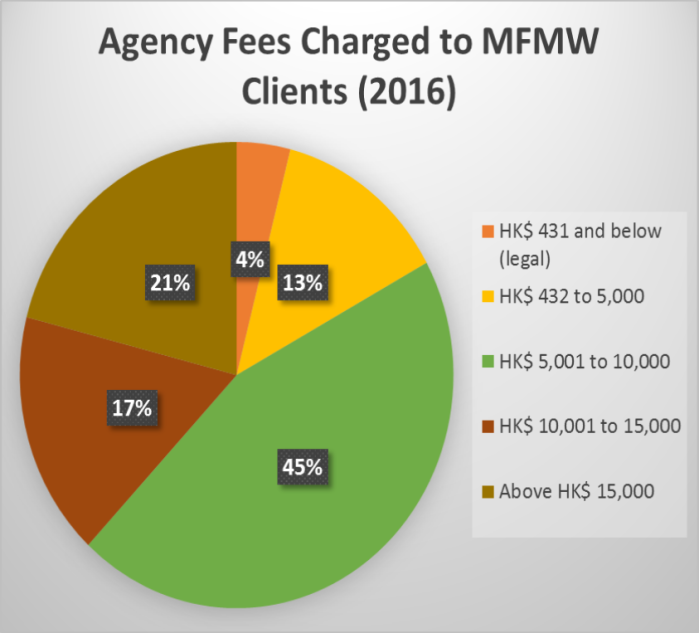

According to the recruitment ordinance in HK, the maximum commission by the recruitment agencies that can be collected from workers is 10% of the first month’s wage upon successful deployment. Currently, this is HK$431.

However, employment agencies would charge the domestic workers in other names like registration fees or training fees. This practice, though widespread, is plainly illegal.

This problem is compounded by debt bondage. These fees usually take the form of fraudulent “personal loans” by the worker but are taken as payment by the agencies. The deceptive practice tends to evade the Hong Kong cap on agency commissions but result in workers paying 5 –7 months of their salaries. – MFMW Service Report 2016

“There are a lot of moneylenders around them here in Hong Kong, both legal and illegal. Domestic helpers usually turn to these companies and individuals so they can send some money in the Philippines. Some illegal moneylenders, like what was reported last month, ask for the helpers’ passports before they can be granted loans,” she added.

On March 12 – 13, 2017, Hong Kong’s Organized Crime and Triad Bureau arrested a local couple and eight Filipina maids for charging illicit interests to money lent to domestic helpers. Authorities confiscated some 242 passports, work contracts, and other evidences.

The Philippine Consulate General in Hong Kong prohibits Filipino citizens from using their passports as loan collaterals and deactivates the travel document if used.

Easy Money, Difficult Consequences

When Precious borrowed money from a registered credit company in Hong Kong for the hospitalization of her husband and child, her loan was approved instantly.

“At first I was hesitant to make a loan because I heard stories about other domestic helpers who got into trouble because of unpaid loans,” said the 27-year-old former-nurse-turned-domestic-helper.

But her need was urgent, and she can’t find other ways to save the lives of her family so she applied for a HK$ 13,000 loan from a financing company. She was asked to submit a photocopy of her employment contract, her passport and Hong Kong ID, her address and telephone number in the Philippines and in Hong Kong, and the telephone number of her employer.

The financing company made an overseas call to the Philippines to verify the telephone number she had given.

“I know one domestic helper here in Hong Kong. She went back to the Philippines while she still has existing loan in Hong Kong. I heard the financing company sent representatives to the Philippines and she was reported to NBI (National Bureau of Investigation). They made a way for her to pay her balance in Philippine Peso,” Precious shared.

Her employers do not know that she has incurred a loan here in Hong Kong. They made it clear from the start that they don’t want her getting indebted to anyone.

“Sometimes, when I am checking my e-mail account, they (employers) would peek and ask where the message comes from. Good thing, I pay the lending company on time so I don’t get notices from them,” she said.

Trina also went to the same process as Precious. The former pre-school teacher was required to submit identification documents and address and contact number in the Philippines. And like Precious, her employers do not know that she availed a HK$ 40,000 loan because they oppose the practice and do not want trouble if she won’t be able to pay.

Although it is relatively easy to avail large-amount loans from moneylenders in Hong Kong, the consequences may be devastating if the loaned amount won’t be paid.

When Maria agreed to help her friend borrow money to a Filipina moneylender she knows, she agreed to surrender her passport as loan collateral. She also agreed to use her name as borrower because the financier doesn’t know the friend personally. When her friend left for Russia without a word, the lender ran after Maria. The harassment and intimidation traumatized her, and when she realized that her husband is having an affair with her best friend back in the Philippines, she almost took her life.

“Good thing, I still have a little sanity left then. I turned everything to God. I was ready to face the consequences then. I thought I will be brought to jail,” Maria recalled.

Upon consultation with the priest of her church, she demanded her passport back, which the financier complied. She said the financier cannot bring her to court because the former charged interest more than what Hong Kong law allows.

According to Ms. Tellez, Hong Kong allows lenders to charge up to 60 percent of the principal amount depending on the capacity of the borrower to pay. Illegal financiers, like Maria’s lender, who charge excessive interests are afraid to file cases in small-claims tribunal because they themselves are violating the law. But harassment and intimidation never stop.

The Philippine Consulate promised Maria that they will run after her friend through embassy connections in Russia.

“My biggest mistake is I trusted a wrong person. I learned my lessons now, never trust anyone no matter how friendly they are to you,” she said.

Financial Management and Education Advocacy

Charity foundation Enrich HK saw the need for financial management training and education of migrant workers.

“Our founders saw a trend among domestic helpers in Hong Kong that, for the longest time they are working here, they have a hard time saving money, or at least stabilize their finances, and when they go back to the Philippines after years of working, there are no improvements in their financial status,” said Mendoza.

Enrich started teaching basic financial management literacy such as budgeting and saving, and eventually ventured to business courses and a full program that address the whole financial life of their clients. They call it Financial and Empowerment Education Program.

Mendoza said they also teach the domestic helpers how to properly communicate with their families back home so they won’t be tempted to give in to the requests of their loved ones.

“Some helpers borrow money to show off when they go back the Philippines, and I can’t blame them for that. Hong Kong has a lot of temptations. What we do is we remind them of their goals when they decided to work here,” she said.

They also help domestic helpers who have problems with their debts.

“If legal intervention is needed, we usually refer them to MFMW or HELP (Help for Domestic Helpers), but we do sit down with them and help them assess the problem. In a way, that educates them.”

Mendoza said if a domestic helper is planning to make a loan, she should ask herself if it is necessary and if she has the capacity to pay. Should a helper be entangled with difficulty of paying multiple debts, Mendoza suggests they should pay the one which charges the biggest interest first.

When asked about her idea of ending the cycle of indebtedness among migrant workers in Hong Kong, Mendoza believes that strong law enforcement and regulations on sources of exploitative charges would reduce the cases significantly.

“If the sending country and the host country would have institutional partnerships and hold trainings on financial literacy and management, it would help a lot in alleviating this pressing problem among domestic helpers,” she concluded.

*’Utang’ or ‘Hutang’ is the Filipino and Bahasa Indonesia’s word for debt.